We’re going to be making credit spread trades on Apple. Every time I send you a trade alert, I’ll explain exactly what I’m doing. But in the meantime, it wouldn’t hurt for you to educate yourself on what exactly a credit spread is.

There are two types of credit spreads we’ll be trading.

- Bear call spreads

- Bull put spreads

Credit spreads are market neutral options trades, with a slight directional bias. What this means is that we can profit if Apple’s share price doesn’t move at all. This is called theta decay — basically, our options become more valuable as we get closer to the strike date.

However, while we can make money this way, simply playing theta decay won’t hand us maximum profits. Maximum profits come when we can correctly determine which way — up or down — Apple’s share price will move each week.

These moves don’t have to be extreme. Even a small move in either direction can turn into a nice gain.

So, let’s look at each of the two credit spread types, and see how we’ll be using them in this strategy.

Bear Call Credit Spread

This strategy, known as a bear call credit spread, is a complex, bearish, risk-limited tactic with a ceiling on potential profits. It aims to capitalize on the underlying asset’s price drop before the option’s expiration.

Short call spreads, another term for bear call spreads, are created through the sale of a call option and the simultaneous purchase of another call option at a higher price. This approach seeks to benefit from a drop in the underlying asset’s price prior to expiration. The bear call credit spread also gains from time decay and a reduction in implied volatility.

Market Perspective for Bear Call Credit Spreads

Initiating a bear call credit spread is a move made when there’s a belief that the underlying asset’s price will fall below the strike price of the sold call option by or before its expiration. These spreads are also referred to as call credit spreads, as they generate credit upon opening. The risk is capped at the difference between the spread and the credit received. The break-even point for this spread is the strike price of the sold option plus the net credit. Time decay and a drop in implied volatility aid in making the position profitable. The closer the strike price of the sold option is to the price of the underlying, the more credit is received at the outset of the trade.

Setting Up a Bear Call Credit Spread

Comprising a sold call option and a bought call option at a higher strike, the bear call credit spread’s received credit is its maximum profit. The greatest risk is the spread’s width minus the received credit. The narrower the gap between the strike prices and the underlying’s price, the more credit is obtained, albeit at a higher risk of the option expiring in-the-money. A wider spread between the short and long options yields more premium but also increases the maximum risk and adopts a more aggressive stance.

Entering a Bear Call Credit Spread

A bear call spread involves selling-to-open (STO) a call option and buying-to-open (BTO) a higher strike call option, resulting in credit. Purchasing the higher strike call reduces the overall premium but defines the risk to the spread’s width minus the credit.

For example, believing a stock will stay under $110 at expiration, one might sell a $110 call and buy a $100 call. If this yields $1.00 in credit, the maximum profit is $100 if the stock ends below $50 at expiration, with a maximum loss of $400 if it ends above $55.

Sell-to-open: $100 call

Buy-to-open: $100 call

The nearer the strike price to the stock price, the stronger the bearish inclination.

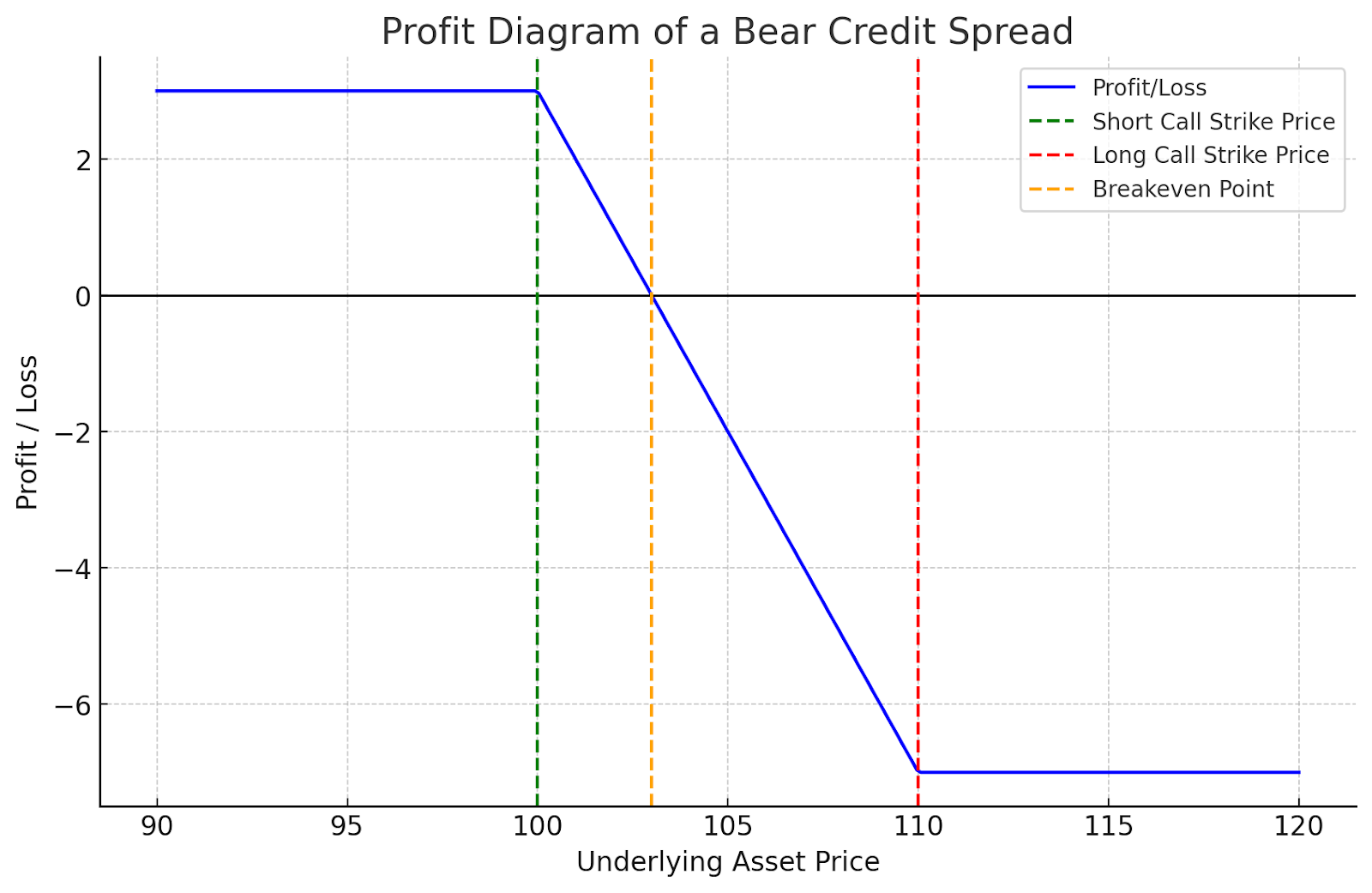

Payoff Diagram for Bear Call Credit Spreads

The key points in the diagram are:

- Maximum Profit: This occurs when the price of the underlying asset is at or below the strike price of the short call (the call option sold). The maximum profit is equal to the net credit received when entering the trade.

- Maximum Loss: This occurs when the price of the underlying asset is at or above the strike price of the long call (the call option bought). The maximum loss is the difference between the strike prices of the two calls, minus the net credit received.

- Breakeven Point: This is the price point of the underlying asset where the trade neither makes nor loses money. It’s calculated as the strike price of the short call plus the net credit received.

The diagram above illustrates the profit and loss scenario for a bear credit spread. Here’s how to interpret it:

- The green dashed line represents the strike price of the short call option.

- The red dashed line indicates the strike price of the long call option.

- The orange dashed line marks the breakeven point.

As the price of the underlying asset decreases (moving left on the x-axis), the profit remains constant at the level of the net credit received, which is the maximum profit in this strategy. If the price of the underlying asset increases beyond the strike price of the short call but stays below the breakeven point, the profit begins to decrease. Beyond the breakeven point, the trade incurs a loss, reaching the maximum loss if the price surpasses the strike price of the long call (red line)

Exiting a Bear Call Credit Spread

Exiting a bear call spread involves buying-to-close (BTC) the short call and selling-to-close (STC) the long call. Profit is realized if the spread is bought back for less than it was sold. If the stock is below the short call at expiration, both options expire worthless, and the full credit becomes profit. If above the long call, the position closes at maximum loss.

For instance, with a bear call spread opened with a $100 short call and a $110 long call, and the stock over $110 at expiration, the broker will automatically transact shares at $50 and $55. If the stock price falls between the calls at expiration, the short option is in-the-money and must be repurchased to avoid assignment.

Impact of Time Decay on Bear Call Credit Spreads

Time decay benefits the bear call credit spread strategy. As expiration nears, the time value of options diminishes. This devaluation may permit buying back the options for less, even without a significant price drop.

Implied Volatility Effect on Bear Call Credit Spreads

These spreads gain from a decrease in implied volatility. Lower volatility leads to cheaper option premiums. Ideally, implied volatility is higher at the spread’s initiation than at its closure or expiration. Future volatility is uncertain but impacts option pricing.

Now, let’s look at the opposite play:

A bull put spread

Bull Put Credit Spread

Bull put spreads, alternatively known as short put spreads, involve credit spreads created by selling a put option and buying another at a lower price. This tactic aims to leverage an increase in the underlying asset’s price prior to expiration. Benefits also include time decay and reduced implied volatility.

Market Perspective for Bull Put Credit Spreads

A bull put credit spread is appropriate when the seller predicts the underlying asset’s price will stay above the strike price of the sold put option by or before expiration. These spreads are also dubbed put credit spreads due to the initial credit they generate. The risk is confined to the spread’s width minus the credit received. The bull put credit spread’s break-even point is the strike price of the sold put minus the net credit. Time decay and a drop in implied volatility aid in profitability. The closer the sold put’s strike price is to the underlying’s price, the higher the initial credit.

Setting Up a Bull Put Credit Spread

This spread consists of a sold put option paired with a bought put option at a lower strike. The received credit is the maximum profit potential. Maximum risk equals the spread’s width minus the credit received. Closer strike prices to the underlying’s value increase credit but also the likelihood of the option ending in-the-money. A wider spread between the short and long options yields more premium, implying a more aggressive outlook and increased maximum risk.

Entering a Bull Put Credit Spread

A bull put spread involves selling-to-open (STO) a put option and buying-to-open (BTO) a lower strike put option, resulting in credit. Buying the lower put option curbs the overall premium but defines the risk to the spread’s width minus the credit.

For example, if an investor believes a stock will remain above $50 at expiration, they might sell a $50 put and buy a $45 put. This could yield a $1.00 credit, with the maximum profit at $100 if the stock ends above $50 at expiration, and a maximum loss of $400 if it ends below $45.

Sell-to-open: $50 put

Buy-to-open: $45 put

The nearer the strike price to the stock price, the stronger the bullish inclination.

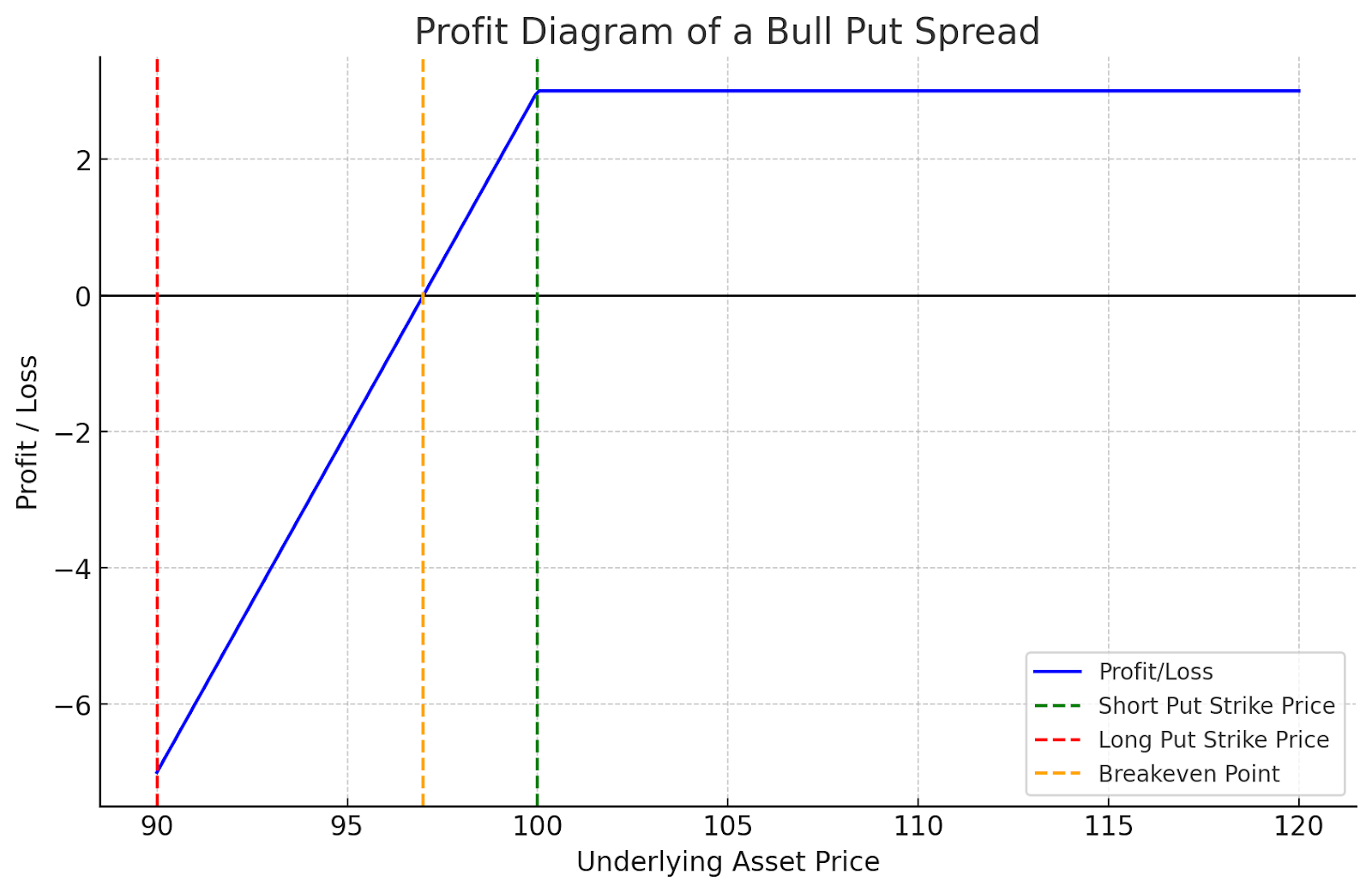

Payoff Diagram For Bull Put Spread Payoff

The diagram above shows the profit and loss scenario for a bull put spread. Here’s how to interpret it:

- The green dashed line represents the strike price of the short put option.

- The red dashed line indicates the strike price of the long put option.

- The orange dashed line marks the breakeven point.

In this strategy, as the price of the underlying asset increases (moving right on the x-axis), the profit remains constant at the level of the net credit received, which is the maximum profit. If the price of the underlying asset decreases below the strike price of the short put but stays above the breakeven point, the profit begins to decrease. Beyond the breakeven point, the trade incurs a loss, reaching the maximum loss if the price falls below the strike price of the long put (red line).

Exiting a Bull Put Credit Spread

Exiting this spread involves buying-to-close (BTC) the short put and selling-to-close (STC) the long put. Profit is realized if the spread is bought back for less than the sale price. If the stock is above the short put at expiration, both options expire worthless, fully realizing the credit as profit. If the stock is below the long put, the position closes at maximum loss.

For instance, with a bull put spread opened with a $50 short put and a $45 long put, and the stock under $45 at expiration, the broker will automatically handle transactions at $50 and $45. If the stock price falls between the puts at expiration, the short option is in-the-money and must be repurchased to avoid assignment.

Time Decay and Bull Put Credit Spreads

Time decay, or theta, favors the bull put credit spread strategy. As expiration nears, the time value of options diminishes, potentially allowing the repurchase of options for less, even without a significant price rise.

Implied Volatility and Bull Put Credit Spreads

These spreads gain from a decrease in implied volatility, leading to lower option premiums. Ideally, implied volatility is higher when the spread is initiated than at exit or expiration. Future volatility impacts, though unpredictable, are crucial for option pricing.

Conclusion

If some of this seems confusing to you, don’t worry. In each trade alert, I explain exactly what I’m doing, and take a copious amount of screenshots. It may seem intimidating at first, but credit spreads aren’t that complex once you’ve traded them a few times.